Investing in your child or grandchild’s future education is one of the greatest gifts you can give—a gift that will last a lifetime and can help open doors to opportunities in the future. With the cost of a college education continuing to soar, it is wise to start saving when kids are young. Saving, even a little at a time, can make a substantial difference down the road.

A state-sponsored 529 College Savings Plan is a tax-smart option for saving for a child’s future education. The money you contribute to the plan grows federal tax-free, and withdrawals are not taxed as long as funds are used for qualified education expenses.

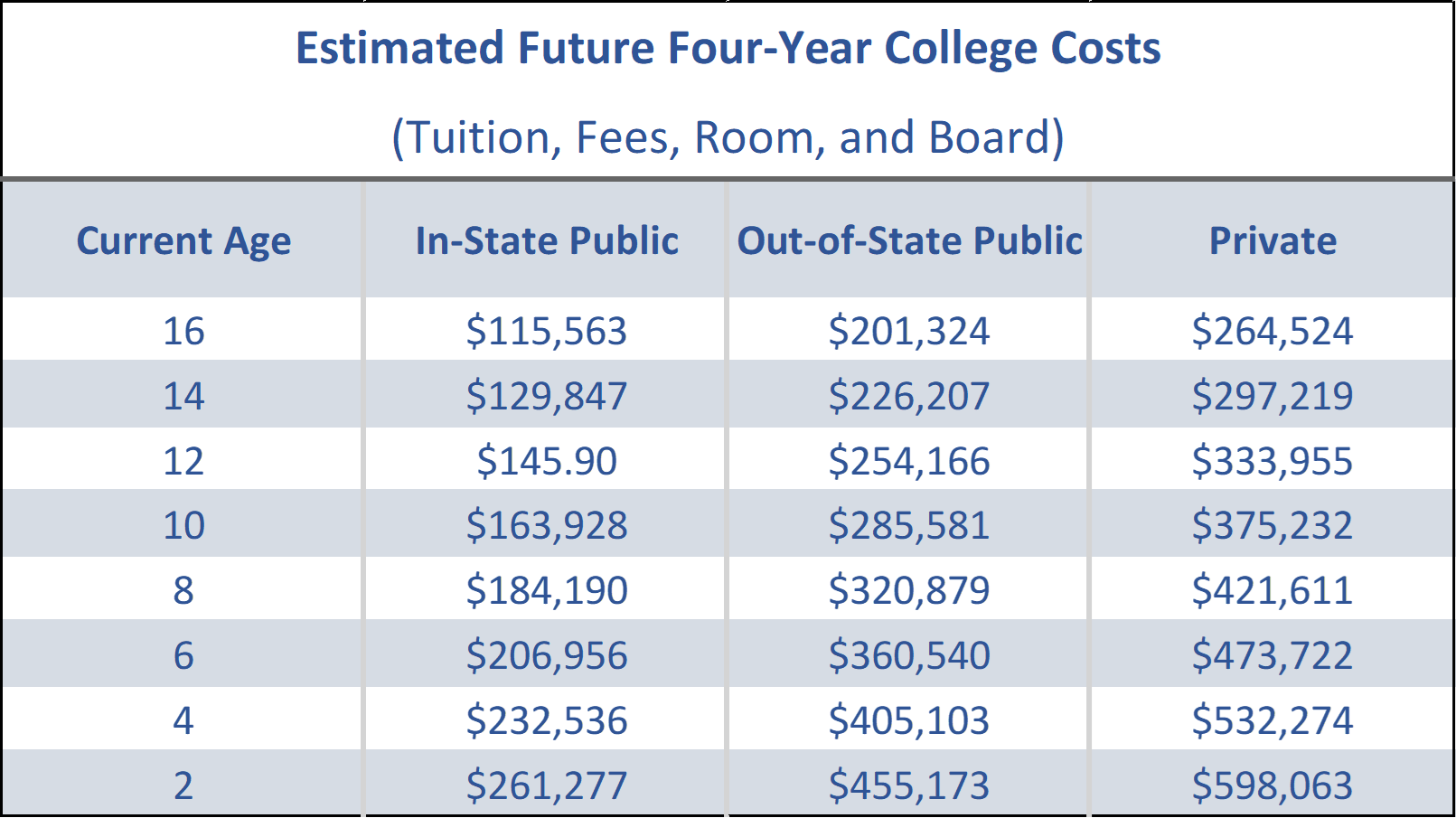

Higher Education Costs Continue to Soar

The numbers are staggering. College costs tend to increase at about two times the rate of inflation each year; a trend that is expected to continue for the foreseeable future.

Here’s what you can expect to pay for four years of college (tuition, fees, room, and board) by the time your kids (or grandkids) are ready to head off to college (assuming a steady 6% college cost inflation rate):

For example, the College Saving Plans Network estimates–at an inflation rate of 6%–that it will cost $261,277 to send a child (who is 2 years of age in 2022) to an in-state public college for four years (including tuition, fees, room, and board). The estimate for private college is a staggering $598,063!

Note: Want an estimate of how much it will cost to send your child or grandchild to college? Use the College Cost Calculator at the College Savings Plans Network.

529 Plans Can Help

One often overlooked college savings option is a state-sponsored 529 Plan. These plans offer great tax benefits, while often allowing you to contribute substantially higher sums than other savings alternatives.

529 Plans come in two forms: 529 College Savings Plans and 529 Prepaid Tuition Plans. Since 529 Plans operate under individual state laws, costs and details vary by state.

- 529 College Savings Plans allow you to save and invest money in vehicles such as mutual funds. The withdrawals can be used by the beneficiary at any accredited institution of higher education nationwide.

- 529 Prepaid Tuition Plans allow you to purchase tuition credits at a participating college or universities at today’s prices. Credits typically can only be used for tuition expenses, not room and board.

A Tax-smart Way to Save for College

Savings in 529 College Saving Plans grow free from federal income tax, and withdrawals remain tax-free as long as they are used for qualified higher education expenses. Many states offer their own additional tax breaks.

Withdrawals from the plan can be used for tuition and fees, textbooks and supplies, room, and board (on and off campus), housing costs, food and/or meal plans, special needs equipment, laptops and software (if required by school for enrollment or classes), and even internet services.

Additionally, funds from the plan can be used for four-year colleges, two-year colleges, vocational, trade schools, graduate school, apprenticeship programs and some other qualified educational programs, as well as travel abroad.

In 2017, the use of 529 Plans was expanded to cover tuition incurred at public, private or religious elementary or secondary schools (limited to $10,000 in K-12 tuition per year), and in 2019 qualified expenses were expanded to allow for paying off student loan debt ($10,000 lifetime limit).

Note: If you take a nonqualified withdrawal from your 529 Plan, you will be assessed a federal 10% penalty and must pay tax—at your tax rate and not the student’s—on the earnings portion of the withdrawal. Some states impose additional penalties.

Investment Options

529 College Savings Plans are like other investment plans—such as 401(k)s and IRAs—in that your contributions are invested in mutual funds or other investment products.

Each state (except Wyoming) has its own 529 College Savings Plan which may vary in structure and investment options (typically mutual funds). Most plans offer a variety of both age-based (or target-date) investment options where the underlying investments become more conservative as withdrawal time nears, as well as risk-based investment options where the underlying investments remain in the same fund(s) regardless of the age of the beneficiary. You are not required to put all your money in one place—you have the option to diversify. While many plans allow investors from out of state, there can be significant advantages for in-state residents.

The minimum investment to open an account and limits on contributions vary by state. Many state plans allow you to set aside as much as $500,000 or more per beneficiary. For example, in California you can open an account with just $25 and name your child, your grandchild, yourself or even someone not in your family as beneficiary. The account balance limit is $529,000, yet the balance can continue to increase, beyond the limit, through investment earnings.

Note: Most plans offer an automatic investment option that withdraws a specified amount of money from your source account at regular intervals (monthly, quarterly, or semi-annually). This makes the process easy and can reduce the impact of a yearly lump sum investment.

Special Estate Planning Features

A unique feature of 529 Plans is that they allow you (per the tax-free gift limit) to contribute to your plan up to $16,000 (up from $15,000 in 2021) out of your estate ($32,000 per couple) annually, per beneficiary. Further, current law allows each account owner to pay up to five years of contributions upfront without triggering gift taxes. That means a couple can contribute up to $160,000 per beneficiary in one year.

Other Considerations

- 529 Plans are one of many options to save for college expenses. Because investment options are limited, trading is restricted to no more than twice per calendar year, and funds can only be used to pay for eligible costs. A good rule-of-thumb would be to save no more than 33-50% of your total expected college expense in a 529.

- Any investment may affect a student’s eligibility for financial aid. Earnings withdrawn from a 529 Plan are treated as income to the child and will show up on the following year’s financial aid application.

- Keep in mind, there is no guarantee that any investment portfolio will achieve its investment goals. The value of your 529 account will fluctuate as the market fluctuates.

In conclusion, with college costs on the rise it is important to start saving early. A 529 College Savings Plan is tax-advantaged investment option that lets families save specifically for the future college costs of their kids or grandkids. Wondering if it is the right savings choice for you? Be sure to talk with your Capital Advantage financial advisor.

Sources:

- College Savings Plans Network. College Cost Calculator. www.collegesavings.org/college-cost-calculator.

- College Savings Plans Network. What is a 529 Plan?. www.collegesavings.org/what-is-529.

- Financial Media Exchange, (2022). 529 Plan.

- Savings for College. What is the Penalty on 529 Plan Withdrawals for Non-Qualified Expenses?.

- www.savingforcollege.com/intro-to-529s/what-is-the-penalty-on-an-unused-529-plan.

- Epstein, A. (2021, October 18). Tips for Creating a 529 Plan.

- Folger, J. (2022, January 10). Tax-Smart Ways to Help Your Kids or Grandkids pay for College.